Assicurazione sulla vita intera:è un investimento intelligente? Comprendere i fatti

Ci sono più di 400.000 agenti assicurativi in questo paese e quasi tutti vorrebbero venderti una polizza assicurativa sulla vita intera. Se acquisti una polizza con premi di $ 40.000 all'anno, la commissione sarà generalmente compresa tra $ 20.000 e $ 44.000 per quell'agente. Come puoi immaginare, tale commissione può essere molto motivante, soprattutto considerando il reddito medio di un agente assicurativo di $ 49.840. A peggiorare le cose, molte delle peggiori polizze offrono le commissioni più alte. Sfortunatamente, la stragrande maggioranza delle polizze vendute viene venduta in modo inappropriato e la stragrande maggioranza di coloro che le vendono sono venditori mascherati da consulenti finanziari.

Come risultato di questo ridicolo conflitto di interessi, gli agenti possono spesso sfatare alcuni seri miti nel tentativo di convincerti ad acquistare il loro prodotto, il che potrebbe spiegare la statistica schiacciante secondo cui oltre l'80% di coloro che acquistano questo prodotto se ne sbarazza prima della morte e i sondaggi di medici reali su questo sito e sul nostro gruppo Facebook mostrano che la stragrande maggioranza di coloro che hanno acquistato polizze a vita intera si pentono del loro acquisto. Se tutto questo è nuovo per te, leggi tutto quello che devi sapere sull'assicurazione sulla vita intera prima di continuare con questo post.

Sebbene la maggior parte dei membri del gruppo WCI FB non abbia mai acquistato un'assicurazione sulla vita intera, tra coloro che l'hanno fatto, il 76% se ne pente.

Caricamento in corso...

I numeri sono simili ma leggermente inferiori nel sondaggio in corso su questo sito (che a differenza del gruppo FB permette il voto di chi vende queste polizze).

Molte persone pensano che io odio l'assicurazione sulla vita intera. In realtà no. Odio il modo in cui viene venduto e chi lo vende in modo inappropriato. Se capisci davvero come funziona e lo desideri ancora, sentiti libero di acquistare quanto vuoi. Davvero non mi influenza in un modo o nell'altro. Ma sono stufo di imbattermi in lettori e ascoltatori che NON CAPISCONO come funziona quando lo acquistano e, una volta che lo capiscono, NON lo vogliono.

Come funziona l'assicurazione sulla vita intera

L'assicurazione sulla vita intera può essere stipulata in molti modi diversi, ma in generale si paga un premio mensile o annuale per un periodo di tempo definito o fino alla morte. Più lungo è il periodo di tempo durante il quale si pagano i premi, più bassi saranno i premi. Ogni volta che muori, il tuo beneficiario riceve i proventi della polizza. Poiché il rimborso di ogni polizza sulla vita intera è garantito se la tieni fino alla morte, i premi sono molto più alti rispetto a una polizza di assicurazione sulla vita a termine comparabile.

Una polizza assicurativa sulla vita intera, come altri tipi di assicurazione sulla vita permanente, è in realtà un ibrido tra assicurazione e investimento. La polizza accumula valore in contanti con il passare degli anni. Quel valore in contanti cresce in modo protetto dalle tasse e puoi persino prendere in prestito il denaro esentasse (ma non senza interessi). Alla tua morte, tutto ciò che hai preso in prestito (più gli interessi) viene prelevato dall'indennità in caso di morte e il resto viene pagato al beneficiario. (Ricevi il valore in contanti o il beneficio in caso di morte, non entrambi.)

Questo aspetto dell'investimento consente a coloro che vendono assicurazioni sulla vita intera di trovare tutti i tipi di motivi creativi per acquistarla e modi creativi per strutturarla. I sostenitori più estremisti potrebbero addirittura sostenere che non hai bisogno di NESSUN altro prodotto finanziario durante tutta la tua vita poiché l'assicurazione sulla vita intera può apparentemente prendersi cura di tutte le tue esigenze, inclusi mutui, prestiti al consumo, assicurazioni, investimenti, risparmi universitari e pensione.

Il problema è che per ogni utilizzo dell’assicurazione sulla vita intera, di solito esiste un modo migliore per affrontare la questione finanziaria. Questo post raccoglie i 38 miti frequenti sull'assicurazione sulla vita intera propagati dai suoi sostenitori.

Mito n. 1:tutta la vita è utile per la protezione del reddito prepensionamento

L'assicurazione sulla vita intera non è il modo migliore per proteggere il tuo reddito, l'assicurazione sulla vita a termine lo è. Prima di andare in pensione, puoi acquistare un'assicurazione sulla vita a termine poco costosa per prenderti cura dei tuoi cari in caso di morte prematura. Una polizza di assicurazione sulla vita a termine a premio di livello trentennale con un valore nominale di $ 1 milione acquistata su un trentenne in buona salute costa $ 680 all'anno. Una polizza vita intera simile costerà più di 10 volte di più, $ 8.000-$ 10.000 all'anno. Si tratta di soldi che non possono essere spesi per le rate del mutuo o per le vacanze, né investiti per la pensione.

Mito n. 2:tutta la vita è il modo migliore per ottenere un beneficio permanente in caso di morte

La vita intera non è il modo migliore per ottenere un beneficio permanente in caso di morte:la vita universale garantita senza decadenza lo è. Ci sono poche persone selezionate che hanno bisogno o desiderano una polizza assicurativa che pagherà alla loro morte, qualunque sia il momento. Ciò può essere utile per alcuni problemi insoliti di pianificazione patrimoniale. Tuttavia, esiste un prodotto migliore che fornisce questo ed è molto meno costoso dell'assicurazione sulla vita intera. Si chiama Assicurazione sulla vita universale garantita senza scadenza . NON accumula alcun valore in denaro ma fornisce semplicemente un beneficio in caso di morte per tutta la vita. Costa solo la metà di un'assicurazione sulla vita intera, quindi non sarai sorpreso di apprendere che la commissione dell'agente su questa vendita sarà molto inferiore.

Chiamami cinico, ma sospetto che potrebbe essere uno dei motivi per cui non hai mai sentito parlare di vita universale garantita senza interruzioni. L'assicurazione sulla vita intera fornisce un beneficio garantito in caso di morte che è PROGETTATO (ma non garantito) per crescere lentamente in modo che se muori al raggiungimento della tua aspettativa di vita o più tardi lascerai dietro di te un po' di più del beneficio in caso di morte della polizza originale.

Prestazioni in caso di morte e inflazione

Una polizza sulla vita intera che ho esaminato di recente prevedeva che l'indennità in caso di morte di una polizza da 1 milione di dollari, acquistata a 30 anni, sarebbe stata di 3,17 milioni di dollari alla morte all'età di 83 anni. Sembra fantastico, quasi come una protezione dall'inflazione dell'indennità in caso di morte. Solo che l’inflazione storica è qualcosa come il 3,1%. Al 3,1%, 1 milione di dollari adesso equivarrebbe a 5,04 milioni di dollari tra 53 anni. Una polizza a vita intera verrebbe devastata da un'inflazione inaspettata, poiché i dividendi sono garantiti principalmente da obbligazioni nominali, i cui valori verrebbero assassinati in un contesto di alta inflazione.

Pertanto l'assicurazione sulla vita intera non è né il modo migliore per fornire un beneficio nominale in caso di morte garantito per tutta la vita, né un beneficio reale garantito in caso di morte per tutta la vita. Allora a cosa serve? Che ne dici di un beneficio garantito in caso di morte che potrebbe aumentare se la compagnia assicurativa avesse voglia di aumentarlo? Saresti disposto a pagare premi doppi per questo? Non la pensavo così.

Mito n. 3:l'assicurazione sulla vita intera offre un grande ritorno sull'investimento

La vita intera non è il modo migliore per investire:gli investimenti tradizionali lo sono. Quando paghi i premi per tutta la vita, una parte del denaro va all'acquisto di un'assicurazione, una parte va alle spese generali e al profitto per la compagnia assicurativa, e una parte va alla commissione per il venditore. Il resto va poi nella parte del valore in contanti della polizza.

Ogni anno, la compagnia assicurativa dichiara un dividendo e se ci sono $ 10.000 nella parte del valore in contanti e il dividendo è del 6%, allora $ 600 vengono accreditati sul valore in contanti. Il dividendo viene applicato solo al valore in contanti, non all'intero premio pagato, quindi il tasso medio del dividendo non è in alcun modo correlato al rendimento effettivo della polizza come investimento. In effetti, il ritorno sull’investimento è generalmente negativo per almeno un decennio. Recentemente ho analizzato una polizza per un maschio di 30 anni in buona salute con un'aspettativa di vita di 53 anni. Il rendimento garantito sul valore in contanti è stato inferiore al 2% annuo DOPO 5 DECENNI .

Anche se si utilizzano i valori “proietti” ottimistici della compagnia assicurativa, si prevede comunque un rendimento inferiore al 5%. In realtà, probabilmente ti ritroverai con un rendimento del 3%-4%. Considerando che bisogna mantenere questo “investimento” per 5 decenni, non sembra una grande compensazione. Se hai decenni da investire, è molto più saggio assumerti maggiori rischi con i tuoi investimenti e ottenere un rendimento più elevato. È probabile che un investimento in azioni o immobili fornisca un rendimento nel corso di decenni compreso tra il 7% e il 12%. 100.000 dollari investiti per 50 anni al 3% annuo diventeranno 438.000 dollari. Se invece crescesse del 9%, ti ritroveresti con 7,4 milioni di dollari, ovvero 17 volte tanto denaro. Il tasso con cui comporti i tuoi investimenti a lungo termine è importante, soprattutto su lunghi periodi di tempo.

Mito n.4:le compagnie assicurative sono grandi investitori

Alcuni agenti credono che le compagnie assicurative possano in qualche modo ottenere rendimenti sugli investimenti che tu o io non possiamo trovare altrove e trasferire questi grandi rendimenti ai loro proprietari di polizze. Può essere illuminante guardare sotto il cofano e vedere cosa c’è realmente nel portafoglio di una compagnia assicurativa. Nel 2016, il patrimonio delle compagnie assicurative era investito per il 67% in obbligazioni (quasi tutte ordinarie obbligazioni societarie e del Tesoro), per l’1% in azioni privilegiate, per il 12% in azioni ordinarie, per l’8% in mutui ipotecari, per l’1% in beni immobili, per il 4% in contanti, per il 2% in prestiti ai titolari delle polizze e per circa il 5% in “altro”. Grazie alla rivoluzione dei fondi indicizzati, un singolo investitore può acquistare quasi tutta quella roba per meno di 10 punti base all’anno in spese. La gestione attiva non funziona meglio per le compagnie di assicurazione che per i fondi comuni di investimento.

Come ci si potrebbe aspettare, i rendimenti di un portafoglio composto principalmente da buoni del tesoro (attualmente con un rendimento dell’1%-2%) e obbligazioni societarie (attualmente con un rendimento del 3%-4%) non sono particolarmente elevati. Allora da dove provengono i dividendi? Una parte viene dal rendimento del portafoglio di investimenti, una parte viene dalle commissioni di coloro che hanno rinunciato alle loro polizze, e una parte viene dai "crediti di mortalità", che sono fondamentalmente soldi che non hanno dovuto pagare ai beneficiari perché sono morte meno persone di quanto avevano pianificato (ovvero, hai pagato troppo per la parte assicurativa della polizza in primo luogo a causa delle normative statali). Non ci sono investimenti magici in cui le compagnie assicurative possono investire che non puoi fare senza la compagnia. Ogni livello aggiuntivo tra te e l'investimento non fa altro che aumentare le spese e ridurre i rendimenti.

Mito n. 5:la vita intera è una grande risorsa

Ci sono molte classi di attività che vale la pena includere in un portafoglio diversificato, ma la vita intera non è una di queste. I venditori di assicurazioni generalmente ricorrono a questo argomento una volta che si rendono conto che non possono convincerti che tutta la vita è un grande investimento in sé e per sé. Dicono che se lo mescoli in un portafoglio di azioni, obbligazioni e immobili migliorerà il portafoglio complessivo. Tuttavia, puoi chiamare qualsiasi cosa tu voglia una classe di attività. Il letame equino può essere una classe di attività, ma ciò non significa che dovresti investire in esso. Pensatela in questo modo. Se ti dicessi che ho una asset class con le seguenti caratteristiche:

- 50% di carico iniziale il primo anno

- Pene di resa che durano anni

- Richiede contributi continui per decenni

- Difficile da riequilibrare con altre classi di attività

- Supportato dalle garanzie di un'unica società (e da tutto ciò che puoi ottenere da un'associazione di garanzia statale)

- Ti richiede di pagare gli interessi per ottenere i tuoi soldi

- Rendimenti negativi garantiti per il primo decennio

- Rendimenti bassi anche se lo mantieni per decenni

- Deve essere conservato per tutta la vita per fornire anche un basso rendimento dell'investimento

- Escluso dall'investimento per cattiva salute o hobby pericolosi

lo compreresti? Ovviamente no.

Mito n. 6:vivere tutta la vita è un ottimo modo per risparmiare sulle tasse

Tutta la vita non è il modo migliore per ridurre le tasse sugli investimenti, i conti pensionistici lo sono. A molti agenti piace pubblicizzare i benefici fiscali dell'assicurazione sulla vita intera, spesso paragonandola a una 401 (k) o a una Roth IRA. Il valore in contanti cresce in modo protetto dalle tasse, il valore in contanti può essere preso in prestito esentasse e i proventi della polizza alla tua morte sono esenti da imposte sul reddito (anche se non sulla proprietà). Quindi alcuni sostenitori della vita intera suggeriscono di utilizzare un'assicurazione sulla vita intera invece di un conto pensionistico come un 401 (k) o un Roth IRA. Tuttavia, un 401(k) o Roth IRA non solo fornisce PIÙ risparmi fiscali e ti consente di investire in investimenti più rischiosi che probabilmente ti forniranno un rendimento più elevato, ma non devi nemmeno prendere in prestito i tuoi soldi, né pagare interessi per il privilegio di farlo.

Ho pubblicato in precedenza sui 3 modi in cui un 401 (k) ti fa risparmiare sulle tasse e su come l'assicurazione sulla vita intera non è come una Roth IRA. Ho anche scritto su come gli investimenti fiscalmente efficienti in un conto di investimento imponibile non comportano quasi il carico fiscale che gli agenti amano dirti di avere. Ci sono vantaggi fiscali nell’investire in un’assicurazione sulla vita? Sì, ma sono drammaticamente ipervenduti.

Mito n.7:l'assicurazione sulla vita intera protegge il tuo denaro dai creditori

Gli agenti assicurativi adorano usarlo sui medici, che possono essere paranoici riguardo ai problemi di protezione dei beni. Tuttavia, spesso non menzionano (o forse non sanno nemmeno) che le leggi sulla protezione patrimoniale sono molto specifiche per ogni stato. Ad esempio [2022] , in Alabama, solo $ 500 del valore in contanti dell'assicurazione sulla vita intera sono protetti dai creditori, ma il 100% del denaro nel tuo 401 (k) o IRA è protetto. Il West Virginia fornisce solo una protezione di $ 8.000. La Carolina del Sud protegge $ 4.000. Il New Hampshire non fornisce alcuna protezione. Molti stati forniscono una protezione del 100% per il valore in contanti dell'assicurazione sulla vita intera, ma probabilmente dovresti consultare le leggi specifiche del tuo stato prima di cadere in questo mito.

Mito n.8:serve tutta la vita per la pianificazione patrimoniale

L'assicurazione sulla vita con valore in contanti ha alcune ottime funzionalità di pianificazione patrimoniale che possono essere molto utili. Tuttavia, la stragrande maggioranza delle persone, compresi i medici, non ha bisogno di queste funzionalità. Il vantaggio principale dell'assicurazione sulla vita è che alla tua morte ottieni un sacco di contanti esenti da imposte sul reddito. Ciò può aiutare con molti problemi di liquidità, come la proprietà di proprietà costose o un’attività privata. Se hai due figli che vuoi condividere equamente nella tua proprietà, e la maggior parte della tua proprietà è la fattoria di famiglia, dovrebbero vendere la fattoria, tagliarla a metà o chiedere a uno di acquistare l'altro per condividerlo equamente. Tuttavia, se avessi anche una polizza di assicurazione sulla vita con lo stesso valore della fattoria, un bambino potrebbe ottenere la fattoria e l’altro potrebbe ottenere i proventi dell’assicurazione. Allo stesso modo, nel fortunato caso in cui si possieda un patrimonio molto grande (più di 5 milioni di dollari per i single secondo il codice fiscale federale, ma può essere molto inferiore in alcuni stati), i proventi dell'assicurazione sulla vita possono essere utilizzati per pagare le tasse sulla proprietà. Ciò sarebbe utile anche nel caso di un unico erede per evitare che venda a prezzi di svendita un immobile o un'azienda di pregio per pagare le tasse.

Ad alcune persone piace anche inserire un'assicurazione sulla vita in un trust irrevocabile per ridurre le dimensioni del proprio patrimonio ed evitare le tasse sulla proprietà. Anche se è possibile inserire nel trust semplici investimenti imponibili (e probabilmente ne uscirebbe vantaggio grazie a rendimenti più elevati), le aliquote fiscali del trust possono essere piuttosto elevate, mettendo seriamente a dura prova i rendimenti per investimenti inefficienti dal punto di vista fiscale, per non parlare del fattore seccatura. È importante sottolineare che non è l'assicurazione sulla vita a risparmiare sulle tasse di successione, ma il fatto che stai regalando i tuoi beni prima di morire affidandoli a un fondo fiduciario.

Tuttavia, il fatto è che la stragrande maggioranza degli americani, compresi i medici, compresi anche i medici con un “problema di tasse sulla successione”, non hanno bisogno di un'assicurazione sulla vita intera per effettuare una pianificazione patrimoniale efficace. La maggior parte delle persone morirà senza alcun onere fiscale sulla successione. Di coloro i cui patrimoni saranno tenuti a pagare alcune tasse sulla successione, la stragrande maggioranza dispone di liquidità che può essere utilizzata per pagare le tasse. Anche se desideri ridurre le dimensioni del tuo patrimonio per evitare tasse sulla successione, puoi farlo facilmente senza acquistare un'assicurazione sulla vita. Tu e il tuo coniuge potete donare $ 16.000 ciascuno [2022:visita la nostra pagina dei numeri annuali per ottenere i dati più aggiornati] a qualsiasi erede in un dato anno senza alcuna implicazione di imposta sulla successione/donazione. Ad esempio, se avessi 4 figli e ognuno di loro avesse 4 figli e tutti i 20 eredi fossero sposati, si tratta di 40 persone. 40 x $ 16.000 x 2 =$ 1,28 milioni all'anno che possono essere prelevati dal tuo patrimonio senza pagare alcuna imposta sulla successione/donazione. Non ci vorrà molto per scendere al di sotto del limite dell'imposta di successione a quell'aliquota, non è necessaria alcuna assicurazione.

Mito n.9:Tutta la vita è un ottimo modo per pagare l'università

Alcuni agenti arrivano addirittura a suggerirti di utilizzare una polizza a vita intera per pagare l'università dei tuoi figli. Puoi farlo? Ovviamente. Basta stipulare prestiti politici e inviare quei soldi all'università per pagare le tasse scolastiche. Ma faresti meglio a risparmiare per il college usando un buon 529 per molteplici motivi. Innanzitutto, spesso ottieni un'agevolazione fiscale statale utilizzando un 529 che non è disponibile per l'assicurazione sulla vita intera. In secondo luogo, non devi prendere in prestito denaro dal tuo 529, devi semplicemente ritirarlo. Nessun pagamento di interessi richiesto. Ultimo, ma certamente non meno importante, considera l’arco temporale dei risparmi universitari. I genitori generalmente risparmiano per il college in un periodo di 5-20 anni. Investendo quel denaro in modo aggressivo, possono aspettarsi un rendimento del 7%-10%. L'assicurazione sulla vita intera ha rendimenti molto scarsi per periodi di tempo inferiori a 20 anni. In effetti, molte volte il rendimento in denaro del tuo “investimento” nell’intera vita è negativo per almeno un decennio. È importante assicurarti che i tuoi soldi lavorino duro come te e che siano in vacanza per il primo decennio in una polizza vita intera. I sostenitori della vita intera sottolineano che se muori, l'indennità in caso di morte potrebbe comunque pagare il college, ma è molto più economico coprire tale rischio con un'assicurazione sulla vita a termine.

Mito n. 10:tutta la vita è il lusso che desideri

Gli agenti assicurativi ricadono occasionalmente su questo argomento quando viene sottolineato che un cliente non ha realmente alcun tipo di bisogno di un'indennità permanente in caso di morte. Ammettono che il cliente in realtà non ha bisogno di un'assicurazione sulla vita intera. Quindi provano a venderlo basandosi sul fatto che sia uno status symbol o un lusso. “Certo, non ne hai bisogno, è un lusso.” Un lusso è per definizione qualcosa di cui non hai bisogno. Preferisco che i miei lussi siano qualcosa che mi piace davvero. Quindi, prima di acquistare un’assicurazione sulla vita intera come un lusso, chiediti:“Cosa mi piace veramente?” Se possiede un'assicurazione sulla vita intera, va bene, comprane una. Ma scommetto che la maggior parte di noi preferirebbe un lusso come una bella macchina, una crociera con i nipoti o magari una donazione a un ente di beneficenza preferito.

Mito n. 11:tutta la vita ti consente di spendere gli altri tuoi beni, offrendoti una preziosa flessibilità in pensione

Tutta la vita non è il modo migliore per assicurarti di non rimanere senza soldi, lo è rendere in rendita alcuni dei tuoi beni. La vita intera non è il modo migliore per affrontare la questione del secondo a morire, lo è invece strutturare adeguatamente le pensioni e le rendite. Agli agenti di vita intera piace inventare scenari di pensionamento che ti facciano sentire come se dovessi possedere o almeno voler possedere un'assicurazione sulla vita permanente, soprattutto per una coppia sposata. Ad esempio, parleranno di una pensione che viene pagata solo fino alla morte del coniuge che lavora. Oppure si parlerà di rendere in rendita una parte del proprio patrimonio in base alla vita di un solo componente della coppia. Quindi suggeriranno che i proventi della polizza sulla vita intera vengano utilizzati per le spese di soggiorno del secondo coniuge morto. Non vi è alcun motivo per utilizzare una polizza vita intera in questo modo. Se vuoi che la tua pensione duri fino alla morte di entrambi, seleziona questa opzione. Se vuoi che la tua rendita duri fino alla morte di entrambi, scegli questa opzione. Sì, pagherà ad una percentuale leggermente inferiore, ma la differenza tra i pagamenti è inferiore al costo di una polizza assicurativa sulla vita intera che coprirebbe la perdita di quella pensione. Semplicemente non è la soluzione giusta al problema. L’assicurazione sulla vita intera offre una certa flessibilità in pensione? Certo, ma il costo di questa flessibilità è troppo alto.

Mito n.12:tutta la vita è un ottimo modo per acquistare cose costose

Tutta la vita non è il modo migliore per comprare cose costose, risparmiare lo è. Ci sono alcuni venditori assicurativi davvero creativi là fuori che sostengono sistemi come Bank on Yourself o Infinite Banking. Lo schema di base è questo:strutturando la vostra polizza in modo appropriato con integrazioni versate, ottenete molto valore in contanti nella vostra polizza nei primi anni, in modo tale da raggiungere il pareggio in 3-4 anni anziché in 8-15 anni. Acquisti anche una polizza di "riconoscimento non diretto". Ciò significa che quando prendi in prestito dalla polizza, la compagnia assicurativa continua a pagare i dividendi sull'importo che era presente prima che tu lo prendessi in prestito, quindi i dividendi della polizza sostanzialmente annullano il pagamento degli interessi dovuti sul prestito. Ora, invece di andare sul tuo conto di risparmio o in banca per prendere in prestito denaro quando hai bisogno di un'auto, di un frigorifero o di un investimento immobiliare, prendi in prestito dalla tua polizza vita intera praticamente a costo zero. Inoltre, il valore in contanti della polizza che non prendi in prestito crescerà più velocemente del denaro in una cassa di risparmio.

Allora qual è il problema? Il problema è che devi acquistare una polizza vita intera di cui non hai bisogno. Potresti andare in crisi anche prima di quanto faresti con una polizza tradizionale, ma ci sono ancora diversi anni di rendimenti negativi e, a lungo termine, gli stessi rendimenti bassi. È meglio guadagnare il 4%-5% all'anno dopo 5 anni o guadagnare l'1% all'anno a partire dal 1° anno? Bene, per i primi 6 o 7 anni stai meglio con il conto di risparmio all'1% annuo. Inoltre, se i tassi di interesse salgono dai minimi storici, rimarrai bloccato in questo sistema per il resto della tua vita. Non è passato molto tempo da quando potevo ottenere più del 5% da un fondo del mercato monetario. Sembra anche molto semplice finanziare un'auto presso un concessionario a tassi di interesse estremamente bassi. Lo 0% o l'1% non sono rari. È meglio prendere in prestito da loro all'1% piuttosto che dalla tua polizza al 5%. La situazione è simile per gli elettrodomestici e i mutui. Fai tutto questo sforzo per poter prendere in prestito da te stesso, poi ti rendi conto che è più economico prendere in prestito da qualcun altro. Infine, se non hai bisogno di effettuare un acquisto per 5 o 10 anni, hai tempo per investire in qualcosa che probabilmente avrà un rendimento molto più elevato di una polizza vita intera. Coloro che puntano su se stessi vengono truffati? Non necessariamente, ma generalmente sono ipervenduti sui vantaggi del loro programma. I suoi sostenitori sono principalmente agenti assicurativi che cercano di aumentare le vendite attraverso il marketing creativo. Risparmiare è semplicemente il modo migliore per fare grandi acquisti rispetto all'acquisto di una polizza sulla vita intera.

Mito n.13:le persone o le aziende veramente ricche acquistano un'assicurazione sulla vita intera, quindi dovresti farlo anche tu

I sostenitori della vita intera, in particolare quelli che sostengono l’utilizzo della polizza come una banca, amano sottolineare che molte persone molto ricche e molte aziende (comprese le banche) acquistano effettivamente assicurazioni sulla vita intera. Sebbene sia vero, è irrilevante per la persona tipica. Le grandi imprese non hanno accesso alle opzioni di risparmio fiscale sui conti pensionistici di cui dispone un individuo della classe media. Gli individui ultra-ricchi li hanno già esauriti. Quando hai molti più soldi di quelli di cui potresti mai aver bisogno, il ritorno sui tuoi soldi non ha molta importanza. Bill Gates può permettersi di investire in qualcosa che fornisce rendimenti del 2%-5% perché non ha bisogno che i suoi soldi lavorino molto duramente. Questo semplicemente non è vero per la stragrande maggioranza delle persone della classe medio-alta, compresi i medici. Come discusso in precedenza, le persone ultra-ricche possono anche avvalersi maggiormente dei benefici limitati di pianificazione patrimoniale e dei benefici di protezione patrimoniale dell’assicurazione sulla vita permanente. In breve, i bassi rendimenti inerenti all'intera vita sono molto meno un problema per loro di quanto lo siano per te.

Mito n.14:dovresti comprare la vita intera quando sei giovane

Ai venditori di vita intera piace sottolineare che la vita intera è molto più economica se la compri quando sei giovane. Sebbene sia vero che i premi sono inferiori se acquisti una polizza a 25 anni rispetto a quando la compri a 55, una volta preso in considerazione il valore temporale del denaro e il fatto che pagherai i premi per altri 3 decenni, non è affatto meglio un investimento in giovane età che in età avanzata. Gli attuari sono persone molto intelligenti e, per un rischio relativamente facile da modellare, come la morte, possono valutare l'assicurazione in modo abbastanza efficiente.

A parte i premi più bassi, ci sono altri due motivi per cui sembra meglio acquistarlo da giovani. Innanzitutto, tale commissione è ripartita su più anni, quindi ha un impatto minore sui rendimenti complessivi. Ma l’alternativa di non pagare affatto la commissione è molto più allettante. In secondo luogo, è possibile che diventerai meno sano o che inizierai qualche sport pericoloso più avanti nella vita. Questo è uno dei gravi svantaggi dell’utilizzo dell’assicurazione sulla vita come investimento:non tutti possono utilizzarla. O non ne hanno affatto i requisiti, oppure il prezzo dell'assicurazione è così alto che il rendimento dell'investimento è addirittura inferiore a quello che sarebbe altrimenti. Non lo vedo come un motivo per comprarlo quando sei giovane, lo vedo come un motivo per non comprarlo affatto. Riesci a immaginare se Vanguard mandasse un paramedico a casa tua per prelevare il sangue prima di permetterti di acquistare il loro fondo S&P 500?

Mito n. 15:la rinuncia ai passeggeri Premium è un buon modo per proteggere la pensione dalla disabilità

L'assicurazione sulla vita intera non è il modo migliore per proteggere il reddito pensionistico dalla tua disabilità, l'assicurazione per l'invalidità lo è. Riconoscendo che i premi dell'assicurazione sulla vita intera sono molto costosi e sarebbero difficili da ottenere in caso di invalidità, le compagnie di assicurazione hanno iniziato a offrire un passeggero che rinunciava ai premi in caso di disabilità. A volte non sembra nemmeno che tu debba pagare un extra per questo vantaggio. Chi cade in questa tattica perde un paio di punti. Innanzitutto, le garanzie non sono gratuite. Ogni garanzia ti costa denaro sotto forma di un rendimento inferiore, sia che la compagnia assicurativa addebiti un extra per la garanzia o che la "inserisca nella polizza" in modo che sia nascosta.

In secondo luogo, l’assicurazione per l’invalidità è complicata e la definizione di invalidità è importantissima. La maggior parte dei medici che desiderano una copertura per invalidità spendono un sacco di soldi per ottenere una polizza davvero interessante con un'ampia definizione di disabilità, inclusa la copertura per "lavoro proprio", perché vogliono assicurarsi che l'azienda dovrà pagare in caso di disabilità. I vantaggi venduti sulle polizze vita intera non sono così completi e hanno molte meno probabilità di essere pagati nelle numerose aree grigie in cui spesso rientrano le disabilità. Quasi sicuramente faresti meglio ad acquistare una polizza di invalidità più grande piuttosto che una rinuncia a vita intera al pilota premium. La tua assicurazione per invalidità può anche offrire una protezione pensionistica. Sebbene anche questi presentino problemi (principalmente nel modo in cui viene pagato il beneficio), sono meglio che cercare di ottenere l'assicurazione per l'invalidità da una polizza sulla vita intera.

Se stai pianificando un pensionamento anticipato come me, potresti renderti conto che non hai comunque bisogno della copertura per invalidità per proteggere i tuoi contributi pensionistici, almeno dopo alcuni anni di forti risparmi. Considera di avere un portafoglio di $ 750.000 all'età di 40 anni. Pensi di aver bisogno di $ 2 milioni in dollari di oggi per la pensione. Prevedi di risparmiare molto in modo da poterlo raggiungere all'età di 50 anni e andare in pensione. Qual è il piano di riserva se diventi disabile e non puoi risparmiare tutti quei soldi? La tua assicurazione per l'invalidità non paga solo fino all'età di 50 anni. Ma paga fino all'età di 65 anni. Quindi non hai bisogno del tuo portafoglio per coprire quei 15 anni. Puoi anche iniziare a ricevere i pagamenti della previdenza sociale quando scadono i pagamenti di invalidità. Dal momento che non devi toccare il tuo portafoglio, può continuare a crescere. Se cresce al 5% dopo l'inflazione, quando raggiungerai i 65 anni varrà oltre 2,5 milioni di dollari in dollari di oggi. Non acquistare un'assicurazione di cui non hai bisogno. Ma anche prima di avere qualsiasi tipo di portafoglio, il modo migliore per proteggere i tuoi risparmi pensionistici è acquistare PIÙ assicurazione per l’invalidità, non cercare di ottenerla da una polizza sulla vita intera. Anche se potessi utilizzare la copertura extra per fornire il tuo portafoglio pensionistico, devi essere in grado di inserirlo in un investimento con un rendimento elevato, che difficilmente tutta la vita fornirà. Un conto imponibile investito in modo aggressivo va bene poiché il tuo reddito principale in caso di disabilità, i benefici dell'assicurazione per l'invalidità, sono esentasse.

Mito n. 16:dovresti scambiare la tua schifosa vecchia polizza sulla vita intera con una nuova brillante

Poiché un agente riceve una nuova commissione ogni volta che vende una nuova polizza, anche se ne sostituisce una vecchia della stessa compagnia, si trova in un grave conflitto di interessi nel formulare raccomandazioni. Interagisco con molti agenti assicurativi su questo blog e nessuno di loro è d'accordo con gli altri su cosa sia una polizza sulla vita intera "adeguatamente strutturata". Ciò significa che se ti rivolgi a un secondo agente, quasi sicuramente ti dirà che esiste un modo migliore per farlo. Tuttavia, perché valga la pena cambiare una politica con un’altra, la politica originale deve essere assolutamente orribile, soprattutto dopo un paio di decenni. La ragione di ciò è che gli scarsi rendimenti delle assicurazioni sulla vita intera si concentrano nei primi anni. Recentemente ho dato un'occhiata a una politica. Questo è stato impostato come investimento con integrazioni versate per i primi 25 anni. È stato il miglior tentativo dell'agente di massimizzare i rendimenti di una polizza. Ecco come apparivano i rendimenti annualizzati:

Garantito Proiettato Primi 10 anni-1,84%0,98%Prossimi 15 anni2,55%5,47%Prossimi 25 anni1,99%5,13%Ciò dimostra che i rendimenti scarsi sono altamente concentrati nei primi anni. Con questa particolare politica, i rendimenti diminuiscono effettivamente dopo 25 anni perché è allora che si smette di effettuare aggiunte pagate. Con una politica più tradizionale la terza fila sarebbe leggermente più alta della seconda. Ma la morale della storia è che dovresti prima acquistare la “politica giusta”, e anche una politica scadente che ha più di 10 anni sarà migliore di una politica nuova di zecca, migliore. Questo è anche il motivo per cui può essere una buona idea mantenere una vecchia polizza vita intera, anche se acquistarla inizialmente è stato un errore. È anche degno di nota vedere quanto poco rischio stia effettivamente assumendo la compagnia assicurativa, dal momento che non garantisce nemmeno che il tuo valore in contanti manterrà il passo con l'inflazione.

Mito n. 17:tutta la vita è l'unico modo per trasferire denaro agli eredi esenti da imposte sul reddito

La vita intera non è l'unico modo per trasferire denaro agli eredi esenti da imposte sul reddito alla tua morte. In realtà, non è nemmeno il modo migliore, lo è un Roth IRA. Quando muori, i tuoi eredi ricevono un'indennità assicurativa in caso di morte esente dall'imposta sul reddito. Ciò che gli agenti spesso non menzionano è che quasi tutto ciò che i tuoi eredi ricevono da te quando muori è esente da imposte sul reddito. Grazie all'aumento della base alla morte, qualsiasi cosa al di fuori di un conto pensionistico, inclusi mobili, automobili, azioni, contanti, fondi comuni di investimento e beni immobili, viene rivalutata il giorno della tua morte. Poiché la base è ora la stessa del valore, non sono dovute imposte sulle plusvalenze. Ereditare un conto pensionistico può essere ancora migliore, soprattutto un conto Roth in cui le tasse sono già state pagate. You can take all the money out the same year you inherit it and not pay any taxes at all. Or, you can “stretch it”, taking withdrawals gradually over decades until you die. Meanwhile, it continues to grow tax-free. You can stretch an inherited tax-deferred account too, but you do have to pay taxes on any money withdrawn from the account.

Myth #18 — With Whole Life, There Is No Way I Can Lose Money

People invest in whole life insurance because they like guarantees. The insurance company guarantees that you'll get a certain rate of growth on your investment and it guarantees a death benefit. The guarantees, however, aren't worth nearly as much as people often assume. For instance, the guaranteed scale of any whole life insurance policy guarantees that your money will grow slower than the historical rate of inflation, despite sticking with it for half a century. Before deciding to trust a single company with your life savings, you might want to consider what happens if it goes out of business. There are state insurance guarantee associations that will cover the cash value and death benefit of your policy, but how much will they really cover? You might be surprised how little it is. In my state, only $500K in death benefit and $200K in cash value is covered, NO MATTER HOW MANY POLICIES YOU OWN. Your state is probably similar. No wonder agents are always talking about the long-term viability of their insurance company. It really does matter! Now I don't think the risk of any given insurance company going out of business in any given year is very high, nor do I think a typical purchaser is likely to end up with exactly the guaranteed growth rate. But before buying, you should realize that investing in whole life insurance isn't the risk free proposition agents like to present it as.

Myth #19 — Life Insurance Should Not Be “Rented”

This one is pretty easy to see through, but you still see agents using it frequently. Since everyone “knows” that it is better to own a home than rent one, the agent says something like “You wouldn't rent your home for the rest of your life would you? So why would you rent your life insurance?” Basically, the agent is referring to the fact that if you use term insurance after age 60 or so, it becomes more and more expensive each year, just like renting a home. But unlike a home, you don't need life insurance after you become financially independent. When you only need a home for a year or two or three, it is a better idea to rent than to buy. When you only need life insurance for a decade or two or three, it is also a better idea to “rent” than to buy. The opportunity cost of “ownership” is simply too high.

Myth #20 — Banks Own Life Insurance So You Should Too

This is a frequent one heard from the Bank on Yourself/Infinite Banking crowd. An underpinning of this school of thought is that the greedy banks are taking over the world so you should only do your financial work through the trustworthy insurance companies. To be honest, I don't have massive distrust for either one of these industries. Both industries have mutually-owned options (mutual life insurance companies and credit unions) where, like Vanguard, the customers own the company. The agents like to point out that banks actually own whole life insurance as part of their “Tier One Capital,” the money used to determine if the bank is adequately capitalized or not. This is somehow to make you fear that the banks know something you don't, like the financial world is about to implode and any of those using banks instead of insurance companies for their financial needs are going to go broke. Tier One Capital is a measure of a bank's financial strength. Banks use less than 25% of their Tier One Capital to buy single premium whole or universal life insurance on a group of employees. The bank owns the policy and is the beneficiary. When the employee keels over, the bank gets the cash. The bank is buying the policy primarily for the death benefit, not because the return is particularly high.

Tier One Capital is highly regulated and it is difficult for a bank to include riskier assets such as common stock(aside from that of the bank, which makes up most of Tier One Capital) and REITs in its Tier One Capital. When you are stuck choosing between low-risk/low-return investments, then you can understand why a bank might consider something like cash value life insurance with part of that money. However, individual physician investors investing for retirement have fewer restrictions on their investment options for their retirement. Most of them have significant need for their retirement money to grow. The returns available with cash value life insurance generally are not high enough for them to reach their goals. Even so, consider what a bank does with most of its Tier One Capital—it buys the only stock it can, it's own. If whole life insurance was so awesome, you'd think the bank would use all of its Tier One reserves to buy it. In short, doctors aren't banks, so doing what banks do isn't necessarily smart. Tier One Capital is highly regulated and it is difficult for a bank to include riskier assets such as common stock.

Myth #21 — Corporate CEOs Own Whole Life Insurance So You Should Too

Agents, particularly of the Bank on Yourself type, love to point out that the golden parachutes for many highly-paid CEOs include cash value life insurance policies. However, just as the financial situation of a bank is dissimilar from that of a physician, so is the financial situation of a CEO making $10 Million a year different from that of a physician. When you're making a gazillion dollars a year, rate of return on your money becomes much less important and thus the benefits of whole life (asset protection, tax, estate planning, etc.) become relatively more important. It isn't that returns on whole life magically get better. Again, if you are in a position that you only need your long-term money to grow at 3%-5% nominal per year, then feel free to invest in whole life insurance. Most of us, however, need higher growth. Remember that a doctor making $200,000 per year and a CEO making $10 Million per year are in very different financial circumstances and what works fine for one will not necessarily work well for the other.

Myth #22 — Banks Failed During The Great Depression, But Insurance Companies Didn't

This myth again preys on the fears of a global economic meltdown. In 1933 there were two holidays. The first was a “Banking Holiday” in which the banks were closed for 10 days as sweeping regulatory changes took place. The second was an “Insurance Holiday” in which for a period of nearly six months you could neither surrender your cash value life insurance policies for cash, nor borrow against them. Aside from this holiday, 14% (63 companies) of life insurance companies actually DID fail during The Great Depression. In fact, if they would have actually marked to market the bonds and mortgages they held, they would have ALL been insolvent. Reforms were put in place during The Great Depression that fixed many of the problems leading to bank failures and the banking holiday. However, these reforms were never put in place for insurance companies.

Myth #23 — After-Tax, Whole Life Returns Are Better Than Bond Returns

This one usually goes like this. “If you can buy a bond yielding 5% and are in a 45% marginal tax bracket, the after-tax yield on that is just 2.75%. A whole life policy with a “tax-free” internal rate of return of 5% is better.” This is an apples to oranges comparison. What is the 1 year return on that whole life policy? 2.75% sounds a whole lot better to me than a -50%. Even at 10-20 years, the bond is still way ahead.

I wrote about a physician who was pleased with his 7% return on his whole life policy bought in 1983 (don't expect to see that again any time soon). Except that he could have bought a 30-year treasury that year yielding 10.5%. 10 years later, as his whole life policy is breaking even and interest rates have dropped, the bond purchaser has not only already more than doubled his money just from the coupon payments, but the capital gains on that bond added another 50% to his return. That investor would have done even better purchasing equities in 1983, the start of an 18 year bull market. A bond, which can be sold any day the market is open, simply cannot be compared in any fair manner to an insurance policy which must be held for life to have any decent kind of return. Besides, most physician investors can hold taxable bonds inside retirement accounts instead of a taxable account anyway. That retirement account not only provides for tax-protected growth like a whole life policy, but also a tax-rate arbitrage between your marginal rate at contribution and your effective rate at withdrawal, further boosting returns.

Even if your only choice is between buying bonds in a taxable account and buying whole life insurance, keep in mind that even at today's low interest rates you can still buy Vanguard's Long-Term Tax Exempt Muni Fund yielding 3.17% [2014] . The guaranteed return on whole life insurance cash value, held until your life expectancy, is about 2% and the projected return is only ~5%. Realistically, you should probably expect a return of 3%-4% over the long term on that policy. Of course, if you actually wish to cash out of that policy instead of borrowing from it (and paying interest for the right to borrow your own money), the earnings are just as taxable as any taxable bond fund. And if you want your money in a mere 10-20 years, you're going to come out way behind with the life insurance.

Now, if you really understand how whole life insurance works and you think its unique features outweigh its significant downsides, then feel free to run out and purchase as much as you like. It truly does not bother me. I do not make any money if you buy whole life, nor if you decide to buy something else. However, if you are like most, once you understand it, you won't buy it and in fact, if you already have, you'll probably be looking for the best way to get out of whole life insurance. Don't feel bad. 80% of those who purchase these policies surrender them prior to death, 36% within just five years. You've got to ask yourself why so many people who were apparently intending to hold this product for the next 40 or 50 years suddenly changed their mind. I'm sure it has nothing to do with it being inappropriately sold to the financially unsophisticated by insurance agents facing a terrible financial conflict of interest with their clients. Whole life insurance is a product made to be sold, not bought. It is a solution looking for a problem that exists for very few, if it exists at all.

Myth #24 — Whole Life Insurance Keeps Assets Off the FAFSA

This is one is merely misleading. The statement as it stands is true. The Free Application for Federal Student Aid (FAFSA) does NOT consider whole life insurance cash value as an asset of the student or the parents. The problem is, for the typical reader of this blog, that it doesn't matter. Your income alone will keep your child from qualifying for any need-based college financial aid. So if you buy a whole life policy for this reason, you're likely to be disappointed.

Myth #25 — Term Life Expires Without Paying Anything

Another misleading argument. I'm always surprised to see people fall for this line, but they do. Do you complain when you don't get to use your car insurance for any given six month period? How about when your house doesn't burn down? Or you don't get cancer and get to use your health insurance? Then why in the world would you complain that your term life insurance expires and you're still alive. Term life insurance is pure insurance. If you die, it pays. If you live, it doesn't. As a general rule, since on average insurance must cost more than it pays out (since insurance companies have both expenses and profits), you should insure against financial catastrophes. When it comes to death, the financial catastrophe is dying during your earning years, before you become financially independent. So that's the only time period you need to insure against. Some people only fall halfway for this argument, and buy return of premium term life insurance. The same principle applies, of course. You don't walk away empty-handed when your term life policy expires. You had insurance for the entire term, which is exactly what you needed.

Myth #26 — Whole Life Insurance Is the Perfect Investment

This outright lie comes from the true believers. They argue that whole life insurance is safe, liquid, tax-advantaged, creditor-proof, and offers a competitive return. These half-truths all add up to one big lie. Let's take them one at a time:

#1 Safe

Safe from the cash value going down, perhaps, but not safe from losing money. A huge percentage of whole life insurance purchasers lose money because they cancel the policy at some point in the first 5-15 years before they break even on their “investment.”

#2 Liquid

I guess it's more liquid than owning a website or a rental property, but it pales in comparison to the liquidity available in a savings account or a mutual fund that can be liquidated any day the market is open. Even inside retirement accounts, there is absolute liquidity after age 59 1/2, and fair liquidity even prior to that date. Most of the time with whole life insurance you don't even get your money, you just have the right to borrow against it at pre-set terms. You can get that with a HELOC.

#3 Tax-Advantaged

Few understand just how minor the tax advantages of whole life insurance are. There is no up-front deduction like a 401(k). Unlike a real investment, there are no capital gains rates if you surrender a policy with a gain and you cannot deduct the loss if you surrender it with a loss (the usual case). You don't get to use depreciation to reduce the tax burden of your income like with real estate. Instead of being able to withdraw the money tax-free like with a Roth IRA, you can only borrow against the policy, and that's tax-free but not interest-free, just like borrowing against your house, car, or mutual fund portfolio. Sure, you don't pay taxes on the “dividends,” but that's because they're actually a return of premium (i.e., you paid too much for the insurance). The only real tax break associated with life insurance is that the death benefit is tax-free. But that isn't any different from any other investment, where you get the step-up in basis at death. In addition, whole life can't be stretched like an IRA. The tax benefits, such as they are, are limited to a single generation.

#4 Creditor-Proof

Too few docs understand just how low the risk of needing this protection actually is. I calculate my risk of being successfully sued for an amount above policy limits at 1 in 10,000 per year. Maybe half that now that I'm practicing half-time. So should I be so unlucky as to be that one person, I would declare bankruptcy and be left only with protected assets. In my state, that's my retirement accounts, my spouse's assets, $40,000 in home equity, and whole life insurance cash value. Your state may or may not protect whole life insurance cash value. Please actually check if you are so paranoid to actually buy whole life insurance for this reason.

#5 Competitive Return

Mi stai prendendo in giro? Competitive with what? Whole life insurance generally has a negative return for 5-15 years (sometimes more than 30 for really terrible policies). Even a good policy held for 5+ decades only guarantees a 2% return and projects a 5% return.

If I were going to draw up the perfect investment, it would definitely avoid the following characteristics of whole life insurance

- Guaranteed negative return for years

- Requirement to interact with and pay a commission to an insurance agent

- Requirement to give samples of body fluids and submit to a medical exam

- Requirement to answer pesky questions about my health

- Requirement to avoid risky activities

- Requirement to pay interest in order to use my own money

It only qualifies as an “okay” investment in certain very limited situations. It's not even close to a perfect one.

Myth #27 — Insurance Agents Are Just People

This is one of my favorites to see in any sort of discussion with an insurance agent about the merits of whole life insurance. It usually comes when I point out that my problem with whole life insurance isn't so much the product as the way in which it is sold. Obviously, many of them take that quite personally since they've dedicated their life and career to selling this product inappropriately. So they point out that there are bad doctors or that insurance agents are just people trying to make a living. I don't have a problem with the sales profession. I don't even have a problem with people earning commissions for selling stuff. Cindy gets paid on commission to sell ads right here at The White Coat Investor. But if you seek advice from Cindy about whether buying an ad at The White Coat Investor is a good idea for you, you're a fool. Insurance agents are just people and people respond to incentives. An insurance agent has a huge incentive to sell you a whole life policy. The commission on a policy is 50%-110% of the first year's premium. Now you know why he's trying so hard to sell you a big fat doctor policy.

Myth #28 — No 1099 Income with Whole Life

This was a new one to me. I thought I had heard every possible argument for buying a whole life policy until someone whipped this one out. How much trouble is it for you to deal with a 1099? It takes me about 30 seconds using Turbotax. Certainly not a reason to favor one investment over another. Remember not to let the tax tail wag the investment dog. Your goal isn't to minimize your taxes or maximize your tax-free income. It's to have the most money AFTER paying the taxes due.

Myth #29 — What Does The White Coat Investor Know? He's Just a Doctor, and Probably a Crappy One

Sometimes agents start with this argument, but frequently this is where they end, with ad hominem attacks. Sometimes it's phrased like one of these:

So, exactly how does being an ER doctor qualify you to give financial and insurance related advice?

Do everyone a favor and stick to studying medicine.

You’re young, a doctor and absolutely sure that you know everything.

Obviously, medicine has lots of problems and doctors don't know everything, but if the agent's best argument for whole life insurance is an ad hominem attack, that's a good sign that you should have stood up and walked out a long time ago.

Myth #30 — After Maxing Out a 401(k) and Roth IRA, Isn't Whole Life Insurance the Only Tax-Sheltered Option Left?

This is the wrong question to be asking, but the answer to it is still no. Just because it is the only option presented to you by an insurance agent, doesn't mean it is the only option. Other options for retirement savings include defined benefit/cash balance plans, an individual 401(k) for self-employment income, a spousal Roth IRA, your spouse's employer-provided accounts, and Health Savings Accounts (HSAs). In some ways doing Roth conversions and paying off debt is also tax-sheltered. But most importantly, there is no limit on investing in a non-qualified mutual fund account (where long-term gains and qualified dividends are somewhat sheltered from taxes) or in real estate (where income is sheltered by depreciation and capital gains can be deferred indefinitely by exchanging).

Obviously investing in whole life insurance compares better to investing in a taxable account than to a retirement account (where there is no comparison from a tax, investing, or in most states an asset protection standpoint). But the real problem with this argument is that it is focused entirely on the idea that any tax-advantaged investment is always better than any fully taxable investment. That simply isn't true. It also mixes up the idea of an investment and an account, two things that financially naïve doctors sometimes have a hard time telling apart. (Think of the accounts as different types of luggage and the investments as different types of clothing.) The real question to ask yourself when you hear this argument is “Where should I invest after maxing out my available retirement accounts?” The answer is a taxable, non-qualified account. Now you're left with the question of what long-term investment to invest in—tax-efficient mutual funds, real estate, or whole life insurance? It's pretty hard to really compare the merits of those three investments and end up choosing whole life insurance given its limitations and terrible returns previously discussed.

Myth #31 — The Estate Tax Exemption Could Go Down

The idea behind this argument is a rebuttal to the argument discussed in Myth #8. In summary, that argument is that you need whole life to avoid estate taxes, which is silly given the vast majority of doctors won't owe any federal estate taxes. The next step is for the agent to argue “Well, the estate tax exemption might be decreased.” Well, I suppose that's true. Congress can change any law they want any time they want. But buying insurance or investing based on what could happen seems foolhardy. I mean, it is probably just as likely that the estate tax is eliminated as the exemption reduced. It seems to me the best way to plan for the future is to project current law forward, since most laws aren't going to be significantly changed. If they are, you can make changes at that point. At any rate, it isn't like whole life insurance is some magic panacea to eliminate estate taxes. The only reason whole life insurance reduces your estate taxes is by making sure you have less money due to its low returns! The thing that reduces the size of your estate is the irrevocable trust you put the insurance into, and you don't even have to put insurance into it if you don't want to.

Myth #32 — Whole Life Insurance Protects from Nursing Home Creditors

This one was particularly fun to debunk. Apparently, the idea here is to not pay for your own nursing home care somehow by purchasing whole life insurance instead of mutual funds. I'm not sure exactly how those envisioning this process think it will go. Maybe they think the nursing home doesn't ask for money until after you die or something, which is, of course, completely silly. But I think what they're referring to is the ability to spend down your assets to Medicaid levels, get Medicaid to pay for the nursing home, and still be able to leave a huge inheritance to your heirs because Medicaid somehow doesn't look at the value of your whole life insurance.

The whole process of Medicaid planning is a little distasteful to me to be honest. The idea is to hide someone's assets from the state so that the heirs can have them, foisting the cost of caring for the owner of those assets on to the public. But even assuming that you have no ethical problem with doing this, it's unlikely to work very well. Medicaid is state law, so it varies by state, but in Utah, a person can have up to $2,000 in countable assets and still qualify for Medicaid. Above that level, no Medicaid until you spend down to that level. If there is a spouse, the spouse can keep 100% of assets up to $24,720 and 50% of assets up to $123,600. Above that, Medicaid won't pay for the nursing home. Non-countable assets in Utah include:

- Your home if your spouse lives in it

- The value of one vehicle (including a Tesla)

- Funds set aside for a funeral

- Household and personal items

- Cash value of your life insurance policies IF the total face value of all policies is <$1500

So I guess if you want to hide money from Medicaid in Utah, then you could go buy a $1,000 whole life policy. Most states have similar policies regarding cash value life insurance. Even if there were a state with a higher limit than Utah, this seems silly for someone who should spend her entire retirement as a multimillionaire to be making plans to spend down to Medicaid levels for nursing home care. A far better plan to stiff your fellow Utah taxpayer (assuming you have a spouse who doesn't need care) is to upgrade your house and your car.

Myth #33 — WCI Doesn't Understand the Opportunity Cost of Borrowing Against Whole Life Insurance and Investing Elsewhere

This statement has been made without explanation, but the idea isn't that complicated (nor misunderstood by WCI). You can borrow against the cash value in your whole life policy and use that money for whatever you want. You can spend it or you can invest it. Lots of whole life fans use fun phrases like “velocity of money” to describe buying a whole life policy, borrowing the money out, and investing it in something else. The really talented salesmen get you to invest it (along with any home equity they can get you to borrow out) in yet another insurance product.

Is there a cost to not maximally leveraging your life in this manner? Sure, anytime you can borrow at a lower rate and earn at a higher rate you'll come out ahead. But leverage works both ways, and the risk is not insignificant. What is not often mentioned by those advocating doing this is the opportunity cost of plunking money into a low return life insurance policy and buying unneeded death benefit instead of a higher returning investment. For instance, consider two options. You can invest $10K a year into an investment that returns 10% per year or you can buy a whole life policy that won't break even for 10 years. After 10 years, the first investment is worth $175K and the whole life policy only has a cash value of $100K. That's a $75K opportunity cost that apparently the “insurance agent doesn't understand.”

With a properly structured policy, you can break even in perhaps five years (maximizing the use of Paid-Up Additions), and using the combination of wash loans (interest rate to borrow against the policy =dividend rate of the policy) and a non-direct recognition policy, this idea becomes “not terrible.” You still have the opportunity cost of the first few years in the policy, but that is balanced out by a higher return on your cash in later years. I have discussed “Bank on Yourself” or “Infinite Banking” previously in detail if you are interested. It's not an insane use of whole life insurance, but it isn't for me. If you really understand how it works (it's going to take working through a lot of hype to do so) and want to do it, go for it.

Myth #34 — Buy Whole Life Insurance for the Long Term Care Rider

In recent years, insurance companies are adding on a Long Term Care rider to whole life insurance policies (and universal life policies and annuities) and agents are using the fear of expensive long term care to sell them. I find this appalling. Not only are you mixing insurance and investing, but you're now combining two different types of insurance policies with investing. Given the track record of insurance companies with long term care, I think most of my readers should strive to get a place where they can self-insure the risk of long term care, but even if they cannot, I'd prefer a simpler long term care policy on its own than mixing it with an otherwise unnecessary and expensive insurance policy.

The benefit of buying this as a rider of a whole life policy is that the premiums of the policy are guaranteed—you don't have the risk of the insurer upping the premiums like you do with a long term care policy or upping the cost of the underlying insurance like you do with a universal life policy. Those guarantees are worth something.

Remember we're not talking about just an accelerated death benefit. This is just another way of self-insuring long-term care, but with a lower return on the investments used to pay for it. You're really buying two policies combined into one. But there's no free lunch here. You're either paying more for the combined policy, or you're getting less of something, usually death benefit. Most likely, you're also paying for a life insurance policy you don't need or wouldn't otherwise buy. That death benefit isn't free. The reason life insurance companies stopped selling long term care insurance and started selling these hybrid policies is that their actuaries were convinced they are more likely to make money that way. That profit has to come from you, there is no other possible source.

If you do decide you wish to purchase some sort of long term care insurance policy, it is entirely possible that a hybrid product is right for you, but just like health and disability insurance, the devil is in the details. Read the fine print and be sure you know what guarantees the insurance company is actually providing. Know about what is covered, what isn't covered, and whether benefits are indexed to inflation or capped. Or better yet, live like a resident for 2-5 years out of residency so you'll be rich enough to self-insure this risk and never have to make this decision.

Myth #35 — We Don't Say Put All Your Money into Whole Life Insurance

This argument is simply bizarre, but used by agents once the prospective buyer has refused to buy the massive policy they were offered at first. A small commission is better than no commission, I guess. Of course, you shouldn't put all your money into whole life insurance, that's a straw man argument. Also, if buying a policy is a bad idea, you're going to be better off if you buy a small one than a big one. But that's hardly a reason to buy a policy in the first place. Like any asset class, if it isn't a good idea to put a significant chunk of your portfolio into it, it probably isn't a good idea to put any of your money into it.

Myth #36 — Yes, We Have a Few Bad Eggs But Most of Us Are Ethical

This argument is used when I point out that literally hundreds or even thousands of my readers have been sold clearly inappropriate insurance policies. The problem is there are two options to explain this phenomenon. The first is that these agents are unethical. The second is that they're incompetent. Given the statistic that 80% of policies are surrendered prior to death and 76% of the docs I've surveyed regret their purchase, this is hardly just a “Few Bad Eggs” doing this. It's an industry-wide problem.

Myth #37 — You Should Buy Insurance to Preserve Insurability

This one is used to sell insurance to people that don't even have a need for insurance. The idea is to prey upon their fear of the combined risk of needing insurance AND not being able to purchase it. One example would be a 25-year-old single doc with no kids. No life insurance need here. “But what if you get diabetes before you get married and have kids? You should buy the policy now.” Uhhhh . . .no.

First, you may never have dependents.

Second, if you do need it, you'll probably be able to buy it at that time at a reasonable price.

Third, if you do become less insurable, you will still likely have options for some insurance through an employer or other groups.

Fourth, even if you become uninsurable through anyone, the risks must be multiplied. For example, let's say there's a 5% risk of you becoming uninsurable before you have a real insurance need. And the risk of you dying before reaching financial independence is 5%. To get your true risk of a financial catastrophe, you must multiple those risks. 5% x 5% =0.25%. That is a 1 in 400 chance. Life is risky. You can't eliminate every possibility of something bad happening to you and even if you could, that wouldn't be a wise use of your money. Wait to buy insurance until you have a need for that insurance.

This argument is often even extended to children. If you're buying life insurance from the same company that sells you baby food, you're probably doing something wrong. Now, if you could buy a lot of future insurability for that kid very, very cheaply, that might be something to consider. Unfortunately, you can't really do that for several reasons:

First, you have to actually buy unneeded insurance. That newborn likely won't have any need at all for life insurance for 25-30 years.

Second, you're not pre-buying the policy that kid will need. You can't buy the right to buy a 30-year level term policy at age 30. You have to buy a whole life insurance policy. Which means you're also paying for insurance that will be unnecessary on the far end of life too, after the kid has become financially independent.

Third, you generally can't buy enough insurance, or even enough future insurability, to actually meet any sort of realistic life insurance need. Most of these infant policies are only $10K or so. That's basically a burial policy, and as sad as it would be to bury your kid, it's not a financial risk my readers should need to insure against. (I've even heard the argument that you should buy the policy so you can take a few months off work because you'll be too distraught to work, but that's what an emergency fund is for.) Even if you find a policy that allows you to purchase future insurability for a larger policy, let's say $500K, that's not going to mean much in 30 years when the life insurance need actually shows up for the first time, much less in 50 years when the kid is actually reasonably likely to die. At 3% inflation, $500K today will only be worth $200K in 30 years and $109K in 50 years. Better than nothing, but you went to all this effort and expense to preserve insurability and your kid still ended up with inadequate life insurance coverage.

Myth #38 — Whole Life Insurance Is a Great Investment to Put in Your Defined Benefit/Cash Balance Plan

I had this one pitched to me by a doc turned financial advisor of all people. The argument was that you could buy whole life with pre-tax dollars and then if you wanted to pull the policy out of the defined benefit plan you could do so. He felt this was an “advanced technique” for “high net worth folks.” I was flabbergasted. It was such a stupid idea I couldn't believe it. A defined benefit/cash balance plan already provides tax protected growth and asset protection, two reasons frequently cited to buy whole life insurance. You're now paying twice for those benefits. To make matters worse, should you die while this policy is in the defined benefit plan, part of the death benefit becomes taxable, negating another usual advantage of life insurance—a completely tax-free death benefit. But the main reason why this is such a stupid idea is when it comes time to close the defined benefit plan, which is usually done every 5-10 years or so in order to roll it into an IRA. At that point, you have to do one of two things.

First, you can surrender the policy and move the cash surrender value into the IRA. But what is the investment return on the first 5-10 years of a whole life policy? You break even if you're lucky. Not exactly a great investment for that time period, especially compared to a typical conservative mix of stocks and bonds.

Second, you can purchase the policy from the plan. Of course, you have to do that with AFTER-TAX dollars. So while you initially bought it with the pre-tax dollars in the plan, eventually you're going to have to cough up after-tax dollars for the policy. And then what are you left with? A whole life policy you probably neither want nor need and perhaps even with associated premiums you have to make each year. Some deal!

Myth #39 — More Money Is Passed Through Life Insurance

This myth showed up in a comment on a post on this blog. I thought it was particularly creative, especially with the way it was combined with Myth #8 (You Need Whole Life to Help For Estate Planning) and Myth #25 (Term Life Expires Without Paying Anything):

More money is passed through life insurance than any other way. I’ve seen too many people out live term which is throwing money away and need life insurance and are at that time in life uninsurable. Life is really used well in estate and trust planning.

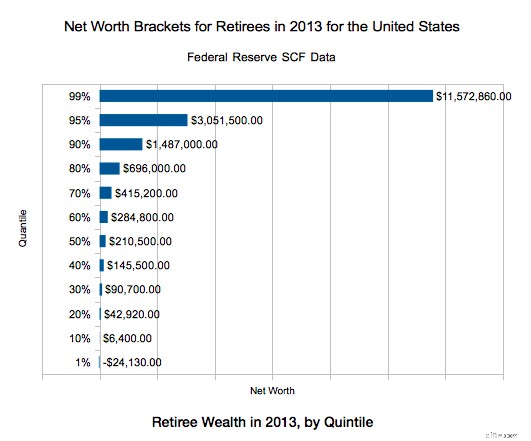

Surprisingly, this was the first time I had heard this argument. Being financially literate, of course I was able to immediately debunk it, but I suppose somebody might fall for it. There are two problems with this statement. First, it may not even be true. I looked and looked and looked for a study that showed what assets are actually inherited, without finding anything that actually quantified it. So if there is a study that actually says this, I suspect it is paid for by a life insurance company. Maybe it's true, maybe it's not, but I suspect it isn't given how few people have life insurance in force at their death. I suspect more money is left behind in houses than anything else. I mean, look at the net worth of people by age. Among retirees, the 50th percentile for net worth is $210K. That's got to be mostly house. The 80th percentile is $696K. That's about the average price of a house in my upper middle class neighborhood in a flyover state.

That jives with the average estate left behind at death:

- The average retired adult who dies in their 60s leaves behind $296K in net wealth,

- $313K in their 70s, $315K in their 80s

- $283K in their 90s

It seems very unlikely that the main inheritance most people receive is the proceeds of a life insurance policy given those numbers. How many retirees even carry life insurance? According to this, about 65% of those 65+. But 47% of those own less than $100K of life insurance. It is a well known statistic that fewer than 1% of term life insurance policies pay out. It isn't that the insurance companies aren't good for the money, it's just that people out live the term. A lesser known statistic is that 80%-90% of whole life insurance policies don't pay out either. They're surrendered prior to death, often at a loss since 1/3 of policies are surrendered in the first 5 years and over half in the first 10 years.

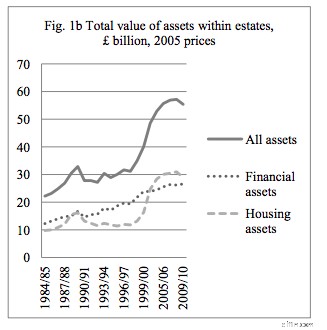

I did manage to find some UK data, however, which suggests my hunch (that people inherit more in real estate than life insurance proceeds) is correct.

As you can see, more than half of inherited assets are housing assets, so clearly more assets cannot be passed as life insurance than anything else.

Perhaps the agent wasn't referring to the median inheritance though. Perhaps he was referring to the total amount of dollars passed to heirs. I could find no data to support nor refute that notion.

Second, even if the statement is true, it is irrelevant. Given that THE PURPOSE of life insurance is to pass assets on to heirs, that's hardly an argument to buy life insurance for some reason besides the death benefit. As I've always said, if you want a life long death benefit that gradually increases throughout your life, then a whole life insurance policy is a great way to get that (although a guaranteed universal life policy can provide a level life long death benefit at about half the price and is probably a better solution for those who really need a permanent death benefit). Bear in mind that you are likely to leave a larger inheritance by investing in stocks and real estate than buying life insurance due to the higher returns, and those assets, just like life insurance, provide a tax-free inheritance to your heirs. Life insurance only provides a larger inheritance if you die well before your life expectancy.

Myth #40 — You Get an Investment and Life Insurance

This one confuses a lot of people and they get really mad when they realize how whole life insurance works. They mistakenly believe that they get a death benefit for their heirs AND a separate “cash value” investment type account that they can use themselves or leave for their heirs. What they do not realize is these two pots of money are one and the same. That which you use for yourself does not get passed on to your heirs. When they discover this fact, they feel like the insurance company is stealing a bunch of money from them and their heirs.

In reality, when you borrow against your life insurance policy, you are borrowing against your death benefit. When you die, your heirs get the death benefit minus any outstanding loans. The amount of the outstanding loans, of course, can never be more than the cash surrender value of the policy, which gradually grows to an amount very close to the death benefit at your life expectancy. So really the cash value just tells you how much of the death benefit you can borrow at any time. You can either borrow this pot of money (death benefit/cash value/surrender value) and spend it yourself, surrender the policy and spend the money, die and leave the money to your heirs, or some combination of the above. But there isn't two pots of money. There isn't a $400K cash value and a $1M death benefit. There is just a $1M death benefit. If you spend $400K of it, your heirs only get $600K of it. So you don't get an investment AND life insurance, you get an investment OR life insurance.

Summing It Up

Ecco qua. Forty reasons for buying whole life insurance debunked. Non preoccuparti; the agents who sell this stuff will come up with more. Just hang out in the comments section over the next year or two and you can watch. Whole life insurance is a product designed to be sold, not bought and the only way to win an argument with an agent trying to sell it to you is to stand up and walk away. As Upton Sinclair famously said, “It is difficult to get a man to understand something, when his salary depends on his not understanding it.” Maybe it should be called Whole LIE Insurance.

Whole life insurance is a terrible investment if you don't hold on to it to your death. Since the vast majority of people surrender their policies prior to death, it is a terrible investment for the vast majority of those who purchase it. If you want to invest in it, then you need to place a very high value on its unique aspects and not mind it's serious downsides.

The ideal purchaser of whole life insurance should:

- Need or desire a guaranteed, but possibly slowly increasing, life-long death benefit,

- Understand that the guarantee/contract essentially relies on the insurance company staying in business for as long as he lives for any policy of reasonable size,

- Live in a state that protects 100% of the cash value from creditors,

- Have some estate planning liquidity issues,

- Be in excellent health,

- Pursue no dangerous hobbies,

- Not mind having low returns on his investment despite holding it for decades,

- Have serious philosophical aversion to using traditional financing resources such as banks and credit unions (or simply just saving up for what you want to buy),

- Have already maxed out all available retirement accounts including backdoor Roth IRAs and HSAs, and

- Be willing to hold on to the policy until death no matter what changes in his financial life in the future.

The fact is that only a tiny percentage of the population, far smaller than the number of people who have been sold these policies historically, meets all or even most of these criteria. Whole life insurance remains a product designed to be sold, not bought.